How the Exodus Strategy Works

It's not hype. It's math and practical strategy.

The Exodus Strategy helps homeowners reduce interest

by keeping their balance lower…for more days each month.

The Mortgage Interest Fact Most People Never See

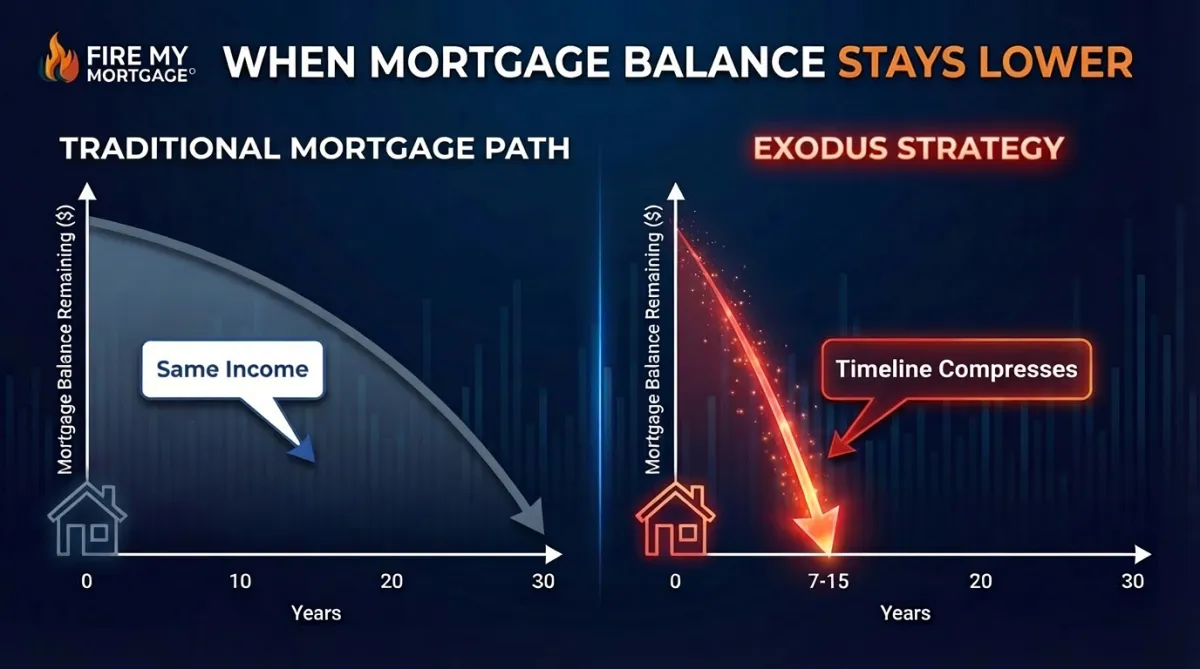

Most mortgages calculate interest daily, based on your remaining loan balance.

That means the amount of interest you pay isn’t determined only by your monthly payment. It’s determined by how high your balance stays during the month.

When the level stays high, interest drains faster.

When the level drops sooner, interest slows down.

Our goal is simple: Keep the level lower more days each month.

Once you understand the mechanics, the strategy becomes clear.

The Exodus Strategy Focuses

on Balance Level

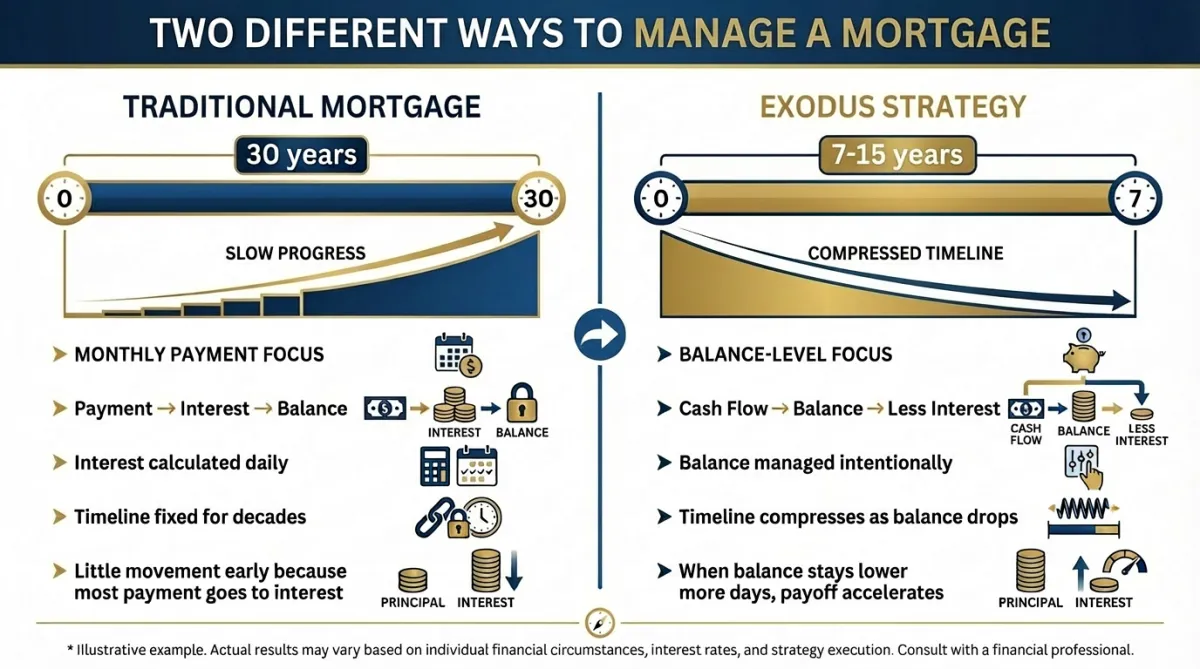

Traditional mortgage thinking focuses on the monthly payment.

The Exodus Strategy focuses on something different:

If focuses on the level of the balance...and how long it stays there.

By improving cash-flow awareness, strengthening financial stability, and using smarter timing, homeowners can keep their loan balance lower more often.

When the level stays lower, daily interest slows — and the payoff timeline begins to compress.

The Three Stages of the Exodus Strategy

Step 1 - Clarity

We start with understanding how daily interest works and how money flows through your household.

The Tools used:

Mortgage Snapshot

Interest Mechanic

Cash-Flow Map

Step 2 - Stability

We strengthen your financial foundation to help ensure the strategy doesn't create stress.

Focus areas:

Financial Buffer

Spending Clarity

Breathing Room

Step 3 - Accelerate

Once stability exists, we begin using cash-flow timing to shorten the life of the mortgage.

Methods may include:

Balance Timing

Strategic Lump Payments

Cash-Flow Optimization

But only when the household is ready

When Interest Slows, the Timeline Moves

Traditional mortgage thinking focuses on the monthly payment. The Exodus Strategy focuses on something different:

How long your balance stays high. By improving cash-flow awareness, strengthening financial stability, and using smarter timing, families can keep their loan balance lower more days each month.

When the balance stays lower, daily interest slows down — and the mortgage timeline begins to compress. We don’t guess.

We model options so you can see what works best for your household.

Illustrative example. Actual results depend on individual finances and modeling.

We Don't Tell You What To Do

Fire My Mortgage® doesn’t push products or demand specific financial decisions.

Instead we help you:

Understand the System

Explore possible paths

Model the numbers

Then you choose what works best for your life.

We model options.

You choose the safest next step.

Clarity is Easier With a Guide

Many Families prefer to walk the journey with a coach.

Our Certified Freedom Strategists are hear to help.

Understand the strategy

Use tools, calculators, and learning paths designed to help you see your situation clearly.

Map their plan

Learn how different strategies affect cash flow, risk, and flexibility — without jargon or sales pressure.

Stay on track

Choose if and when a conversation makes sense for you, based on clarity — not urgency.

See What This Could Look Like For Your Household.

When the pressure of debt goes down, something powerful happens:

Every mortgage is different.

Start by modeling your numbers and exploring what’s possible.

Real Families

Different families. Same starting point.

Listen to how the narratives are changing.

Part of a Larger Mission:

Fire My Mortgage® is part of a broader effort to help families build lasting stability and generational strength through it's participation in the Freedom Framework

Fire My Mortgage helps families create clarity and control using math-based strategies and guided support.

Quick Link